Introduction

As India’s textile and processing industries increasingly move toward higher-performance and compliance-driven chemicals, Biopol Chemicals positions itself as a focused specialty chemical manufacturer.

Let’s explore this upcoming IPO further:

Biopol Chemical’s share price will be finalised post-allotment, while grey market cues through the Biopol Chemical’s IPO GMP will likely reflect market sentiment closer to listing.

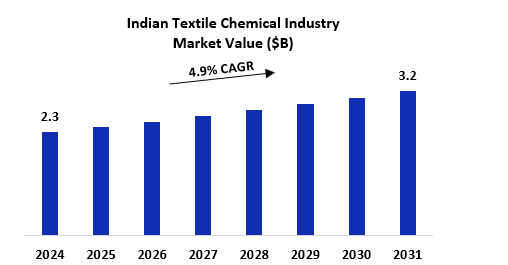

The Industry Backdrop: India’s Textile Chemical Market

India's textile chemical industry plays a crucial role in transforming raw materials into high-quality products used globally. Chemicals such as silicones, polymers, softeners, and emulsions play a crucial role in processes like dyeing, printing, and finishing, enabling fabrics to gain softness, durability, and special features like water resistance.

With India's textile exports booming and a push for sustainable practices, this sector is growing fast. It supports major hubs in Gujarat and Maharashtra, blending local innovation with global demand to shape the future of apparel and technical textiles.

The market stood at around $2.3 b in 2024 and is projected to reach $3.5 b by 2033, growing at a 4.9% CAGR, driven by export surges, technical textile adoption, and domestic manufacturing hubs.

Company Origin Story

Originating in 2005 in Gujarat, the business was initiated as a sole proprietorship under the name United Chemical Company by its promoter, Mr Santanu Sarkar. After nearly two decades of operations in the chemical manufacturing space, the business was restructured and incorporated as Biopol Chemicals Limited in April 2023.

The company is engaged in the manufacturing of speciality and performance chemicals, primarily used in textile processing and industrial applications. Its product range includes textile auxiliaries and speciality formulations, supplied to domestic customers and select export markets. The company operates on a business-to-business (B2B) model, catering to institutional clients rather than retail end-users.

Let’s understand the products made by the company

The product portfolio of the company consists of 66 products, which comprises 40 silicone-based products, 5 emulsifier-based products, 15 biochemical products, and 6 polyelectrolyte products.

These products are used in applications across various industry segments, including softeners, emulsions, and hardeners for textiles; silicone fluids and cleaning chemicals for home care; silicone adjuvants and surfactants in agriculture; and release agents in industrial chemicals.

Names of some of the major chemicals Biopol makes:

• SOFTEX 100

• UNIQO 500

• AQUAPHIL 2020

• SILICONE OIL BIOPOL 1281F

• BIOPOL PDMS 1000.

BIOPOL FUEL OIL

BCL BULK BITUMEN VG 30

In simple terms, these chemicals support processes from pre-treatment to dyeing, printing and finishing, including specialised applications like garment wet processing for denim and other textile finishes.

Capacity: How Much Can Biopol Really Make?

Biopol’s manufacturing facility is a two-storied unit located in Kolkata, West Bengal, with a ground floor of approximately 5,000 sq. ft. and a first floor of 900 sq. ft.

The manufacturing unit is equipped with reactors, mixers, homogenisers, blenders and other process equipment, enabling us to manufacture our range of speciality chemical products.

(*adjusted)

The data shows a clear improvement in capacity utilisation, rising from 61% in FY23 to over 93% in FY24 and FY25, indicating strong demand and better operational efficiency. With utilisation still high at ~87% in 9MFY26, Biopol appears to be running close to its capacity, supporting the need for future expansion while also pointing to limited near-term headroom.

(*Note: It must be noted that apart from manufacturing, the company is also involved in the trading of such chemicals and generated over 33% of total revenue in Fy25)

Financial Performance

The top line has given a high growth of around 60% CAGR from FY23 to FY25. At the same time, the growth in FY25 has been at 93%. The growth, as per 9MFY26, seems to be slightly muted in terms of annualised growth.

Margins have improved moderately, with EBITDA margins expanding from to 8.1% in FY23 to 13.3% in FY25. The PAT margins have risen from 2.7% in Fy23 to 8.8% in Fy25. The management claims expansion in the trading business, along with a reduction in finance costs.

The CFO, however, has continuously been on the negative side in past years, and was recorded at (2.3) Cr in Fy25.

Coming to the cash conversion cycle, being at 117 days in Fy25, has more than doubled in the past two years. As per the management, extension of credit terms and accumulation of inventory are the primary reasons for such an increase.

Biopol Chemicals has significantly reduced its debt level. D/E ratio has dropped from 3.7 in Fy23 to currently at 0.6.

ROE and ROCE stand at 38.1% and 30.6%, placing Biopol Chemicals above the listed peers. The company has also maintained its current ratio well over the years, currently at 1.8.

Peer Analysis (FY25)

On the basis of peer analysis, it can be said that Biopol Chemicals has an average quality of financials.

The EBITDA & PAT margins are currently at 13.3% and 8.8%, respectively, which are at the lower end of the industrial range.

The return ratios of the company are currently higher, with ROE & ROCE at 38.1% & 30.6%, respectively.

In terms of valuation, Biopol Chemicals lies on the fair side with a P/E ratio at 14.6x, while the EV/EBITDA stands relatively higher at around 19.1x. However, it must be noted that the company has higher borrowings, with a D/E ratio of 0.6.

Overall, in terms of margins and valuation, when compared to peers, it can be said that the company has a moderate level of financials, requiring focused efforts by the management.

Management + Promoter Holdings

Biopol Chemicals’ promoter, Mr Santanu Sarkar, brings over two decades of hands-on experience in chemical manufacturing, having operated the business since 2005 through his sole proprietorship, United Chemical Company, prior to its incorporation into Biopol.

The promoter-led management brings strong technical knowledge of speciality chemicals along with practical experience in scaling operations and managing customers, helping the company run at high capacity and serve both domestic and export markets effectively.

While 3 out of 5 board members are independent directors, the governance ensures quality as the audit and remuneration committees are led by independent directors.

From a control standpoint, the promoters hold a dominant 89.9% stake pre-issue. Post-IPO, this stake will dilute to 65.8%, but promoter influence will remain firmly intact, given their high base ownership and board control.

IPO Objectives

The company will be using the proceeds for:

Acquisition of industrial land: The company intends to utilise a portion of the Net Proceeds for the acquisition of industrial land measuring approximately 30,687 square feet situated at Ahmedabad, Gujarat.

Repayment of borrowings: Funds will be used for the partial repayment of borrowings availed by the company from various banks, financial institutions, and non-banking financial companies

General corporate purposes: The remaining Net Proceeds will be deployed toward general corporate purposes, which include meeting operating expenses, supporting strategic initiatives, and addressing business exigencies

Overall, the IPO is primarily aimed at securing land for future capacity expansion rather than immediate growth capex, positioning the company for long-term scaling while maintaining balance-sheet flexibility.

Final Words

At Alpha Venture X Fund, we assess opportunities through our LMVT framework — Leadership, Moat, Valuation, and Tailwinds — enabling us to identify scalable businesses with durable fundamentals.

Leadership: Founder-led with strong industrial experience and equity retention, ensuring aligned execution and focus on scaling the brass components business.

Moat: Despite having in-house manufacturing & a diversified product base, the company lacks a moat as there are various payers involved in silicone-based chemicals.

Tailwinds: Rise in fashion consumption along with China +1 diversification strategy benefiting the Indian textile industry.

Valuation: The company is valued at a fair range, with P/E being at 14.6x; the EV/EBITDA ratio is also on the higher side, currently around 19.1x.

Bottom Line: Biopol has a high revenue growth with moderate financials relative to peers. Textile chemical is a booming industry backed by China +1 strategy & higher domestic consumption. Valuation currently lies in the fair range. Biopol Chemicals is a selective, not an automatic buy.

0

14

0

Publish Date

06 Feb 2026

Category

SME IPO

Reading Time

9 mins

Social Presence

Table Of Content

Introduction

Company Origin Story

Financial Performance

Management + Promoter Holdings

Final Words

Tags

SME IPO

SME IPO Analysis

Biopol Chemicals IPO Review

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2024–2025 Alpha. All rights reserved, Built with ❤️ in India