Decoding India’s Best Performing AIFs

Introduction

India’s investment market is quietly going through a revolution. While mutual funds are still at the heart of retail investing and SIP markets are booming, another segment is quietly building momentum for the next big phase in wealth creation: Alternative Investment Funds (AIFs).

What was once seen as a niche market with high entry costs for investors has now become a new and integral part of wealth creation for high-net-worth individuals, family offices, and institutions. And this is because of only one reason: outperformance.

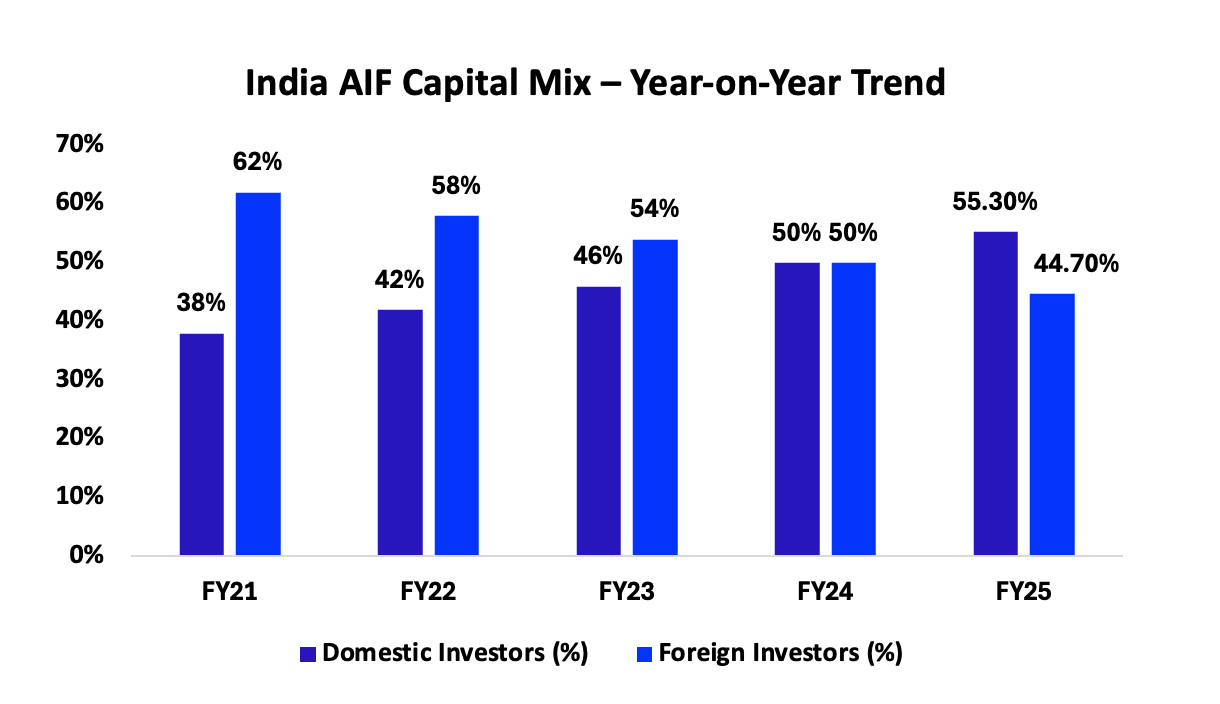

India’s Alternative Investment Funds market, as of December 2025, stands at ₹15.7 lakh crore in commitments and ₹6.45 lakh crore in actual investments, registering a healthy growth rate of 27%+ year-on-year in investments. But more importantly, home-grown investors are now contributing more than 55% to total investments.

But behind these numbers is another, more interesting fact:

There are only a handful of Alternative Investment Funds that are registering returns in excess of 25-35%+ IRR, significantly outperforming market-linked instruments.

The real question, therefore, is not whether Alternative Investment Funds are outperforming markets or not. It is how these top performers are created.

A Structural Inflexion Point: Why AIF Alpha Is Expanding

To appreciate current performance, it’s critical to recognise that we’re not in a cyclical spike; we’re in a structural expansion phase.

In the last five years, AIF commitments have grown at a rate close to 30% CAGR, making AIF one of the fastest-growing segments of the Indian financial system. This is because of three critical changes.

The first change is the emergence of domestic capital, which makes AIF money much more patient.

The second change is the emergence of Category II AIFs, which dominate the ecosystem and represent 60% of the total deployed capital, especially in private equity and private credit, where most 25%+ IRRs are generated.

The third and perhaps most critical change, and the one that’s perhaps most transformative, is the emergence of private credit as a mainstream asset class, which is now close to a ₹2 lakh crore opportunity within AIFs. As traditional lenders exit riskier segments, AIFs have filled the void with structured capital solutions, which are at much higher yields and with much greater equity upside.

What 25%+ IRR Actually Means (And Why It Looks Misleading)

A 25-30% IRR might look like smooth compounding, while in fact, AIF returns are very lumpy and back-ended.

The lifecycle of a fund is normally 6-7 years, with:

The initial years spent deploying capital

The middle years spent scaling businesses and benefiting from valuation mark-ups

The final years delivered most of the returns through exits

So, for instance, a 25% IRR can be driven by just one or two super successful exits, rather than smooth compounding.

This is important to understand, as it gets to the heart of why portfolio construction is more important than performance.

Inside a High-Performing AIF Portfolio

However, if we examine the composition of top performers in the current market, we would find that they are not pure-play funds. Rather, they are funds that offer multiple return engines.

Late Stage/Pre-IPO Equity (35-45%)

This is currently the most powerful return driver for generating exceptional returns. Indian companies are staying private for longer and are now raising capital later in their growth cycle. We are investing at the Series D to pre-IPO stage in companies that have strong revenue visibility and near-term listing potential.

The return driver is:

Investing at a discount to public valuations

Exiting at IPO-driven rerating

This is where we capture valuation arbitrage between private and public markets.

Structured Credit (25–35%): Stability and Upside

Structured credit has become a key driver of alpha returns and is no longer considered a defensive asset class.

Current structured credit products have the following characteristics:

13–16% secured coupon

Equity upside through convertibles/warrants

Downside protection

This produces a blended return profile of 20–28% IRR. The returns have lower volatility.

3. Public Market Special Situations (15-25%)

Top AIFs are also active in public markets, but in a manner distinct from mutual funds.

They are involved in:

QIP and block deals

Pre-IPO and post-listing transitions

Event-driven opportunities

They are free to take large positions in niche opportunities, thus generating alpha where others are unable to.

4. Opportunistic & Distressed (5–10%)

This bucket, though smaller, has become more relevant in recent years.

Tighter credit conditions have created opportunities in:

Stressed assets

Promoter financing

Secondary stake sales

These investments can generate 2–3x returns, disproportionately boosting portfolio IRR.

Real-World Validation: Funds Actually Delivering 25%+ Returns

The framework for this portfolio is not hypothetical, as it is already being executed in real funds.

For example, the Swyom Advisors – India Alpha Fund (Category III) has generated returns of around 31.8% in FY2025, driven by various long-short and high-conviction midcap plays. The fund’s ability to dynamically manage this exposure underscores the power of flexibility in listed markets to create significant alpha in volatile markets.

Another example is Abakkus Emerging Opportunities Fund I, which has generated ~30-32% CAGR over 5 years, making it one of the most visible examples of high-performing AIF compounding. The fund’s strategy is to invest in emerging businesses that benefit from sectoral tailwinds, thus reinforcing that high returns of 25%+ are not just cyclical but can be structurally achieved with the right portfolio construction.

Another example is the Negen Undiscovered Value Fund, which has generated ~40%+ since-inception returns, driven by pre-IPO investments, anchor investments, and special situations. This reinforces another critical point that has been discussed in this series:

The biggest alpha in India today is being generated before companies become widely owned in public markets.

Thus, these examples collectively reinforce the thesis that:

High AIF returns are not just cyclical, but are engineered through access, structure, and timing.

Sectoral Trends: Where the Alpha Is Concentrated

AIF capital is not evenly distributed; it clusters around sectors with scalability and exit visibility.

The most prominent sectors include:

Financial services and NBFCs

Manufacturing and industrial platforms

Consumer and premium D2C brands

Energy transition and infrastructure

These sectors allow AIFs to:

Enter early

Scale with growth

Exit into deep public or strategic markets

The Real Edge: Access Over Analysis

One of the most important insights from analysing top-performing AIFs is this:

Outperformance is driven less by stock picking and more by deal access.

Leading funds benefit from:

Promoter relationships

Proprietary sourcing networks

Investment banking pipelines

Anchor IPO allocations

This creates access to opportunities that are simply not available to public market investors.

Dispersion: Why Most Investors Get AIFs Wrong

Despite strong headline returns, the AIF universe is highly fragmented.

Top quartile funds: 25–35%+ IRR

Median funds: 15–18%

Bottom quartile: Below 12%

This dispersion underscores a crucial point:

In AIFs, manager selection matters more than asset allocation.

Risks in the Current Cycle

As the industry scales, new challenges are emerging:

Rising competition in pre-IPO deals

Regulatory tightening and disclosure requirements

Dependence on IPO markets for exits

Increasing difficulty in deploying large pools of capital efficiently

These risks make execution more complex, reinforcing the importance of experience and network strength.

Why 25%+ Returns Are Becoming More Systematic

Despite all of this, the overall trend remains intact.

High AIF returns are now supported by:

Deeper private markets

Strong domestic capital base

Hybrid strategy execution

Improved regulatory frameworks

As a result, AIFs are becoming repeatable alpha generators, rather than opportunistic.

Final Take: India’s New Alpha Layer

The investment ecosystem in India is getting more and more layered:

Mutual funds provide a return of 10-14%

PMS strategies provide a return of 15-20%

AIFs provide a return of 20-30%

But what is most significant is the difference in terms of time.

Mutual funds invest in identified opportunities.

AIFs invest in opportunities that are either undiscovered or are underpriced.

Closing Insight

The rise of AIFs is, in fact, a reflection of a broader change in India’s markets: from access-driven investing to insight and positioning-driven investing.

For investors who are comfortable with illiquidity, long-term focus, and manager risk, AIFs are no longer just an alternative but are increasingly becoming the main driver of wealth creation in India at an early stage.

And that is what drives those 25%+ returns.

0

0

0

Publish Date

27 Mar 2026

Category

Ideas

Reading Time

7 mins

Social Presence

Table Of Content

Introduction

A Structural Inflexion Point: Why AIF Alpha Is Expanding

Inside a High-Performing AIF Portfolio

Real-World Validation: Funds Actually Delivering 25%+ Returns

The Real Edge: Access Over Analysis

Tags

AIF

NRI

BESTAIF

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2024–2025 Alpha. All rights reserved, Built with ❤️ in India