Introduction

India’s growth narrative is increasingly driven by SMEs, for Non-Resident Indians (NRIs) seeking differentiated exposure to India’s real economy beyond public market beta, the country’s micro, small and medium enterprises (MSMEs) represent both structural scale and institutional inefficiency. With disciplined structuring through SEBI-regulated Alternative Investment Funds (AIFs), NRIs can access governance-led value creation in segments that remain under-penetrated by organised equity capital.

India’s MSME Backbone: Scale, Depth and Structural Importance

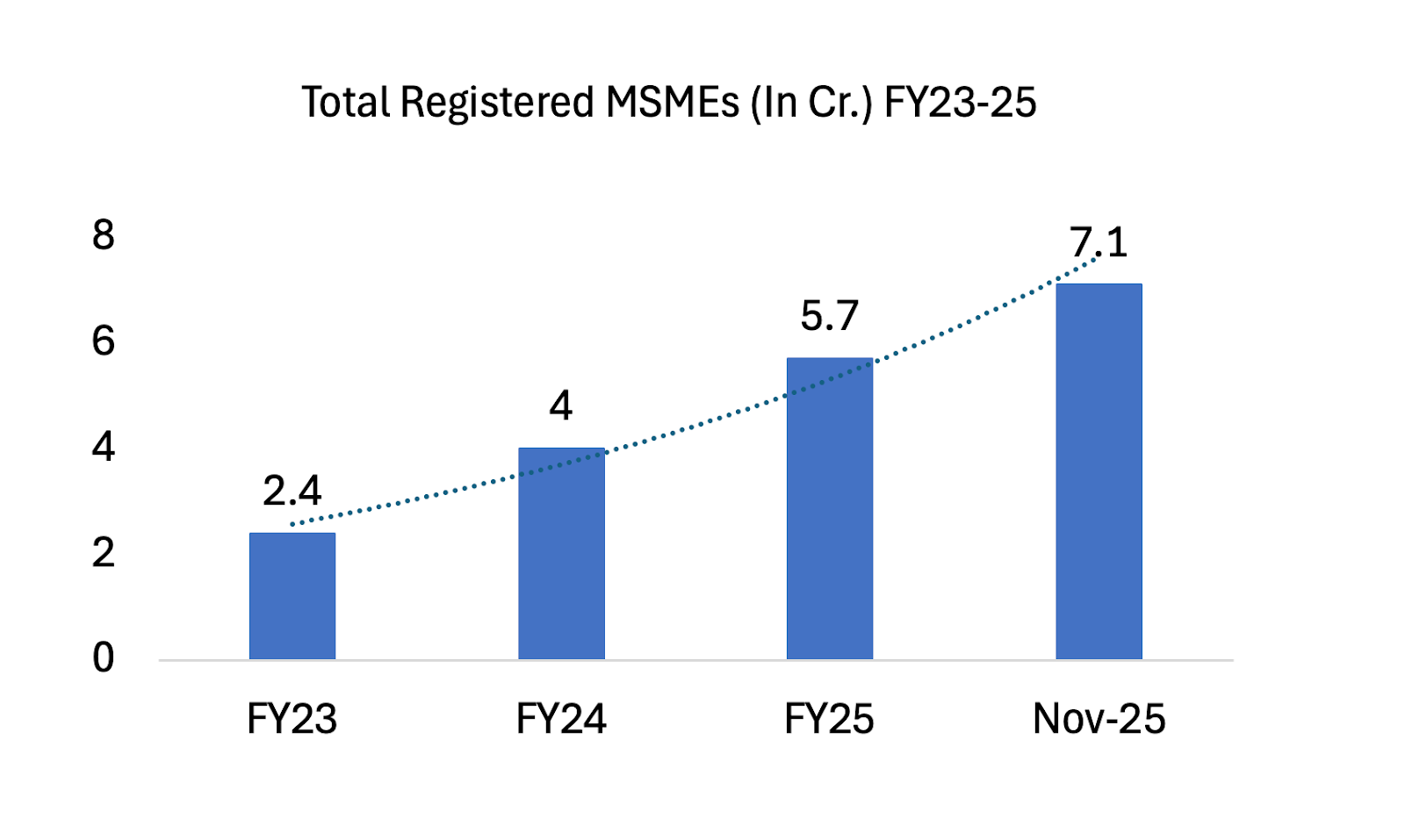

As of 20 November 2025, there were ~ 7.16 crore MSMEs registered on the Udyam Registration Portal and Udyam Assist Platform. These enterprises contribute roughly 30% to India’s GDP/GVA. They account for nearly 45% of India’s exports and support over 110 million jobs. This is not a peripheral segment of the economy. It is foundational.

The sector’s relevance has strengthened under policy initiatives such as the Production Linked Incentive (PLI) scheme and supply-chain diversification trends often described as “China+1,” which have increased domestic manufacturing momentum. Credit flow to MSMEs has also risen meaningfully in recent years as formalisation through GST, and digitisation deepens.

Yet despite this macro significance, institutional equity penetration in lower mid-market businesses remains limited relative to opportunity.

Acceleration in MSME Formalisation

Source: Ministry of MSME, Government of India, Udyam Registration Portal & Udyam Assist Platform data (as on 31 March 2023, 2024 and 2025).

The Capital Formation Gap

Multiple studies have highlighted a significant financing gap in India’s MSME ecosystem. The International Finance Corporation (IFC) has historically estimated India’s MSME credit gap in the trillions of rupees [7]. Policy commentary and industry reports frequently reference an addressable financing shortfall exceeding ₹20 lakh crore+ as of March 2025, varying by year and methodology.

Even conservatively interpreted, the implication is clear: a large portion of India’s entrepreneurial base remains underserved by structured equity and institutional credit capital. For NRIs allocating capital globally, this gap represents inefficiency, and inefficiency is where alpha is born.

The pathway to accessing this segment responsibly lies within the SEBI (Alternative Investment Funds) Regulations, 2012 framework. India’s AIF ecosystem has expanded rapidly over the past decade. As of September 2025, total AIF commitments reached approximately ₹15.05 trillion.

Category-wise capital concentration historically reflects institutional preferences:

Category II AIFs: 75–80% of commitments

Category III: 15%

Category I: 7–10%

While Category II dominates through private equity and credit strategies, Category I funds, which include SME and venture capital vehicles, remain structurally smaller but strategically critical. This is precisely where informed NRI capital can access differentiated opportunity.

The global Indian diaspora is estimated at approximately 32 million people. India remains the world’s largest recipient of remittances, receiving ~ $125 billion+ in 2023–24. However, remittance flows largely serve consumption, real estate and traditional deposits. Institutional SME equity exposure remains a fraction of diaspora capital. A disciplined 1–2% reallocation of diaspora flows toward structured SME AIFs would translate into multi-billion-dollar equity formation annually, without relying on foreign institutional flows.

This creates a compelling strategic question for NRIs: how to access SME alpha while maintaining governance, repatriation clarity and regulatory compliance?

NRIs may invest in SEBI-registered AIFs subject to FEMA compliance, KYC norms and fund-specific eligibility criteria.

Investments are typically routed through designated banking channels (NRE/FCNR/NRO accounts), with repatriation governed by FEMA and RBI guidelines.

Key compliance elements include:

PAN and overseas address proof

FATCA/CRS declarations

Authorised dealer (AD) bank confirmations

Review of fund repatriation clauses within the PPM/LPA

Practical onboarding guides for NRIs investing in AIFs outline these steps in detail.

Risk-Return Characteristics of SME-Focused AIFs

SME growth funds typically target mid-teens to mid-20s gross IRRs, dependent on entry valuation discipline, operational value addition and exit timing.

Unlike venture capital, SME growth funds generally invest in EBITDA-positive companies with established revenue bases. This reduces binary outcome risk while preserving upside through:

Operating margin expansion

Professionalisation of management

Strategic consolidation

SME IPO migration or strategic sale

Liquidity profiles are typically 4–6 years, shorter than early-stage VC but longer than public equities.

For NRIs with long-term capital horizons, the illiquidity premium can enhance portfolio efficiency when structured appropriately.

Alpha AIF

We at Alpha AIF positions itself as a governance-focused SME Category I strategy designed to capture operating leverage in profitable lower mid-market businesses.

The fund thesis centres on:

Targeting companies with ₹15–20 crore+ revenue thresholds at entry

Preference for ROCE above 18% at underwriting

Structured minority or growth capital with board participation

Diversified portfolio across manufacturing and industrial clusters

Sector opportunity is supported by MSME scale data and export contribution.

Alpha’s differentiation lies in:

Local Origination Advantage – Access to tier-2 and industrial cluster businesses underrepresented in mainstream PE pipelines.

Governance Intervention – Board seats, MIS standardisation, and capital discipline to institutionalise promoter-led businesses.

Exit Engineering – Defined pathways including SME IPO platforms, strategic buyers or secondary PE exits.

NRI-Ready Documentation – Structured subscription processes aligned with RBI and SEBI norms.

For diaspora investors seeking transparent structures over informal private deals, this institutional format reduces operational risk.

Portfolio Construction Considerations for NRIs

When evaluating SME AIF exposure, NRIs should assess:

GP commitment (alignment signal)

Management fee and carry structure

Hurdle rate (often ~8% in many PE structures; industry norm)

Independent valuation policies

Audit oversight

Concentration limits

Repatriation clauses

The objective is not thematic enthusiasm but structured risk underwriting.

Public markets in India have deepened significantly over the past decade. However, alpha dispersion has compressed in large-cap segments. SME private markets continue to exhibit valuation inefficiencies, information asymmetry and governance gaps.

MSMEs contribute 30% of GDP and 45% of exports, yet institutional equity participation remains disproportionately small relative to contribution. This structural misalignment supports the case for a measured allocation.

India’s MSME ecosystem, comprising 63 million enterprises, contributing 30% of GDP, and supporting 110+ million jobs, represents one of the largest entrepreneurial networks globally.

Simultaneously, India’s AIF industry has scaled to ₹15.05 trillion in commitments, institutionalising private capital participation under SEBI oversight.

For NRIs, the intersection of these two developments presents a compelling allocation thesis: channelling diaspora capital into professionally managed, governance-centric SME AIFs such as Alpha AIF allows participation in India’s productive capital cycle rather than passive consumption flows. The opportunity is not merely economic.

Disciplined underwriting, regulatory compliance and long-term alignment define whether SME exposure generates sustainable alpha. Through a SEBI-regulated, governance-driven framework, NRIs can move from remittance participants to institutional capital allocators in India’s next growth phase.

0

16

0

Publish Date

19 Feb 2026

Category

Ideas

Reading Time

6 mins

Social Presence

Table Of Content

Introduction

India’s MSME Backbone: Scale, Depth and Structural Importance

The Capital Formation Gap

Risk-Return Characteristics of SME-Focused AIFs

Portfolio Construction Considerations for NRIs

Tags

SME

NRI

GROWTH

NRIINVESTING

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2024–2025 Alpha. All rights reserved, Built with ❤️ in India