Introduction

As India’s e-commerce, logistics, and services sectors lean more on flexible & compliant blue-collar workforces, PAN HR Solution positions itself as a focused staffing partner, combining manpower deployment with payroll and labour-law compliance.

Let’s explore this upcoming IPO further:

PAN HR Solution’s share price will be finalised post-allotment, while grey market cues through the PAN HR Solution’s IPO GMP will likely reflect market sentiment closer to listing.

The Industry Backdrop: India’s Staffing & Recruitment Market

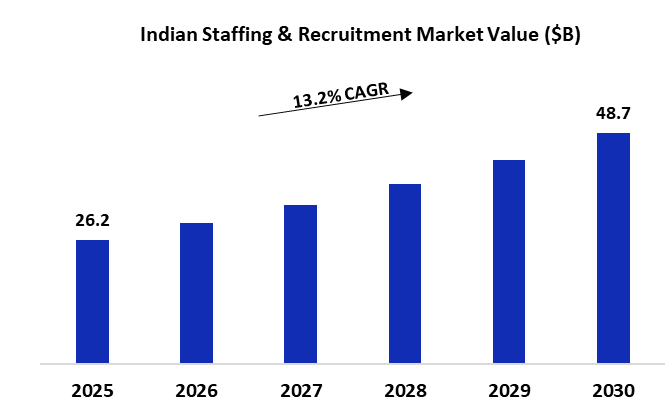

India’s staffing and recruitment industry has grown into a critical enabler for businesses that want flexible, scalable workforces without carrying all employees on their own rolls. Companies across e-commerce, logistics, retail, manufacturing, and services increasingly rely on staffing firms not just for hiring, but also for payroll processing, PF/ESIC compliance, and day-to-day workforce management.

The market is large and fragmented, with a few organised players and many small local contractors. As labour regulations tighten and clients become more sensitive to compliance and reputational risk, demand is gradually shifting towards organised, multi-state staffing firms that can reliably deliver people at scale, manage costs, and stay on the right side of the law.

India's Staffing and recruitment market size was valued at $26.2 B in 2025 and is projected to grow at a CAGR of 13.2% from 2025 to 2030.

Overall, India’s staffing and recruitment industry offers a large, growing opportunity, but without easy moats: it rewards players that can execute consistently at scale, stay ahead on compliance, and manage working capital and client concentration better than the rest.

Company Origin Story

Incorporated in 2015 in Noida, PAN HR Solutions operates on a B2B model and provides comprehensive manpower solutions, catering to a range of roles from unskilled to skilled blue-collar workers. The company has a PAN India presence and provides human resources, staffing services, and compliance solutions to customers in E-commerce, logistics, manufacturing, information technology, and other sectors, enabling them to streamline the hiring process, reduce administrative burden, and ensure suitable candidates.

The company currently operates under a “Collect and Pay” Model, wherein it raises invoices on its Customers/Principal Employers for services rendered in accordance with the applicable terms and subsequently receives payment. The payments are then disbursed to the employees deployed at the client's place.

Industry-wise Revenue %

PAN HR is overwhelmingly an e-commerce staffing story: over FY23–25, more than 80% of revenue consistently comes from e-commerce clients, while logistics has actually shrunk as a share of the mix from 18% to just 8%.

Infra and other categories are slowly rising from negligible to 7%, and manufacturing is still insignificant.

Financial Performance

The top line has given a slow growth of around 5% CAGR from FY23 to FY25. At the same time, the growth in FY25 has been negligible at 0.7%. The growth, as per 9MFY26, seems to be muted in terms of annualised growth.

Margins being at single-digit low, have improved moderately, with EBITDA margins expanding from to 2.1% in FY23 to 2.4% in FY25. The PAT margins have risen from 1.5% in FY23 to 1.8% in FY25. The management claims focus on high-margin work and engagement of lower-salaried personnel as a reason for margin expansion.

The CFO has continuously been on the positive side in past years, and was recorded at 0.8 Cr in FY25. However, it has turned out to be negative in the recent numbers as per 9MFY26.

Coming to the working capital days, being on the negative side over the years, currently at (7) days in Fy25. It must be noted that the company does not carry any inventory, making this financial metric slightly unreliable in terms of evaluation.

PAN HR Solutions carries no debt in its balance sheet, resulting in a D/E ratio of 0 in the current and past years.

ROE and ROCE stand at 31.1% and 38.3%, placing PAN HR Solutions above the listed peers. The company has also maintained its current ratio well over the years, currently at 1.7 in Fy25.

Management + Promoter Holding

PAN HR Solution Limited’s promoters—Mr. Rajeev Kumar and Mrs Rajni Kumari—collectively bring nearly two decades of hands-on experience to the human resource and staffing services industry.

The promoters guide the company by implementing deep operational know-how in comprehensive manpower solutions, recruitment, and talent acquisition, with strong skills in managing large-scale nationwide workforce deployments and navigating the complex regulatory and competitive landscapes of the B2B staffing sector.

While 2 out of 5 board members are independent directors, the governance ensures quality as the audit and remuneration committees are led by independent directors.

From a control standpoint, the promoters hold a dominant 90.9% stake pre-issue. Post-IPO, this stake will dilute to 62.6%, but promoter influence will remain firmly intact, given their high base ownership and board control.

Peer Analysis (FY25)

On the basis of peer analysis, it can be said that PAN HR has an average quality of financials. The EBITDA & PAT margins are at 2.4% and 1.8% respectively, making it the lowest amongst the peers.

The return ratios of the company are currently higher, with ROE & ROCE at 31.1% & 38.3%, respectively.

In terms of valuation, PAN HR lies on the lower side with a P/E ratio at 7.3x, while the EV/EBITDA also stands lower at around 6.1x. However, it must be noted that while peers carry some debt, the company has no borrowings, making a D/E ratio of 0.

Overall, in terms of margins and performance, when compared to peers, it can be said that the company has a moderate level of financials, requiring focused efforts by the management.

Industry Specific Ratios

The table highlights that PAN HR is the most capital-efficient player, with the lowest market cap per person deployed, showing it achieves scale with far less investor capital. It also operates with negative working capital days, indicating faster cash collections.

Happy Square and Armour sit in the middle on both capital intensity and working capital efficiency, while Dynamic Services stands out as the most stretched, with the highest market cap per employee, high receivables, and a long working capital cycle. Overall, PAN HR appears to be the most efficient on both capital and cash management among peers.

IPO Objectives

The company will be using the proceeds for:

Working capital requirements (₹975 lakhs): Funding day-to-day operational needs of the manpower supply business, including timely payment of employee wages, statutory dues (PF, ESIC, GST), and managing receivable-heavy contracts.

General corporate purposes (balance): Supporting business expansion initiatives, strengthening internal systems, meeting compliance and technology upgrade expenses, and covering other strategic and administrative expenses, in line with SEBI norms (limited to ≤15% of gross fresh issue proceeds).

Overall, the issue is to improve liquidity, support scale-up in workforce deployment, and ensure smooth execution of large client contracts while maintaining operational stability in a working-capital-intensive manpower services business.

Final Words

At Alpha Venture X Fund, we assess opportunities through our LMVT framework — Leadership, Moat, Valuation, and Tailwinds — enabling us to identify scalable businesses with durable fundamentals.

Leadership: Founder-led with strong industrial experience and equity retention, ensuring aligned execution and focus on scaling the brass components business.

Moat: The company provides human resources in blue collar worker category. The company lacks a deep and defensible moat, making it vulnerable to competition.

Tailwinds: Growth in e-commerce & logistics creates staffing requirements. However, a rise in automation and industry-wide job cuts may act as headwinds for the company.

Valuation: The company is fairly valued, with a P/E of 7.3x.

Bottom Line: PAN HR solutions operates in low growth industry. The company has given negligible sales growth over the past year and has low margins relative to peers. The company also lacks a moat, providing it with no competitive advantage. PAN HR Solution is not a BUY for investment purposes.

0

11

0

Publish Date

06 Feb 2026

Category

SME IPO

Reading Time

10 mins

Social Presence

Table Of Content

Introduction

The Industry Backdrop: India’s Staffing & Recruitment Market

Financial Performance

Peer Analysis (FY25)

IPO Objectives

Tags

SME IPO

SME IPO Analysis

PAN HR Solutions IPO Review

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2024–2025 Alpha. All rights reserved, Built with ❤️ in India