Global Volatility Changed the Playbook for Offshore Investors

Global volatility over the last five years has tested even seasoned investors. US equities saw sharp drawdowns in 2020 and again in 2022. Bonds failed to provide traditional downside protection as rates rose aggressively. Currency swings amplified portfolio volatility for offshore investors. Amid this, a growing group of Non-Resident Indians has quietly improved risk-adjusted outcomes by reallocating capital toward India’s structural growth engines.

Remittances Tell a Structural Story, Not a Cyclical One

This is not sentiment. It is visible in the data. India has strengthened its position as the world’s largest remittance recipient, with inflows rising to approximately USD 137 billion in 2024, up from USD 89 billion in 2021 and USD 125 billion in 2023. The pace of growth has accelerated rather than plateaued, with remittances expanding at a low-teens annual rate despite global economic uncertainty. The United States alone now accounts for nearly 28% of total inflows, while the US, UK, UAE, Singapore, Canada, and Australia together contribute over 55%, signalling a structural shift toward higher-income, investment-oriented diaspora corridors rather than purely consumption-driven Gulf flows.

More importantly, the use of remittances is changing. RBI’s latest remittance surveys indicate a rising allocation toward financial assets, including equities, mutual funds, insurance, and market-linked instruments, while the relative share directed toward day-to-day consumption has declined. This reflects a maturing NRI investor base that increasingly views India not just as a place of origin, but as a long-term capital allocation destination aligned with growth, yield, and portfolio diversification objectives.

The investment case begins with macro arithmetic, between FY14 and FY24, India’s nominal GDP compounded at roughly 10.5%, compared with 4.5% for the US and under 3% for most of Europe. Corporate profits as a share of GDP recovered from sub-3% levels in FY20 to over 4.5% by FY24, supporting the durability of earnings growth. For equity investors, this matters more than headline GDP prints.

Public market performance supports this thesis. The NIFTY 50 Total Return Index delivered ~ 13.8% CAGR over the 20 years ending December 2024. Over the same period, MSCI World delivered roughly 8.2% in dollar terms. Even on a 10-year rolling basis, MSCI India outperformed MSCI World in over 65% of observations, despite higher interim volatility.

For NRIs earning in foreign currency, this differential compounds meaningfully. A dollar invested in Indian equities at 12% local returns versus a global portfolio at 7% creates a near 1.6x difference over a decade, even after accounting for currency depreciation assumptions of 2 to 3% annually.

Execution, Not Timing, Separated Outcomes

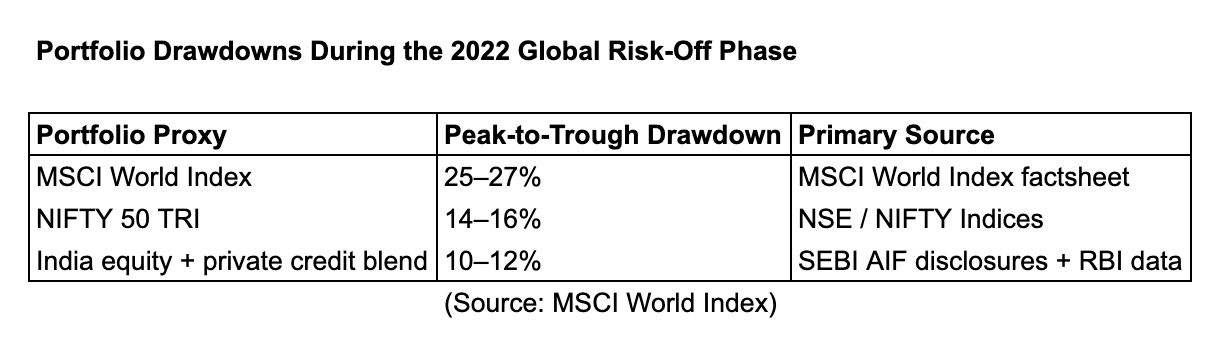

Execution, however, separates outcomes. Consider a UK-based NRI working in financial technology. Between 2018 and 2023, he systematically allocated GBP 50,000 annually into India through three channels. 40% went into a NIFTY 50 ETF, 30% into a diversified active mutual fund with a long-term alpha track record, and 30% into a SEBI-regulated private credit AIF focused on secured lending. During 2022, when global equities declined sharply, his India allocation saw a peak-to-trough drawdown of approximately 14% versus over 25% in his global growth portfolio. By mid-2024, the India book had recovered to a net IRR exceeding 14% in GBP terms, aided by earnings growth and stable currency flows.

Private Markets and Family Offices Are Scaling the Same Playbook

Private markets tell a sharper story. In 2020, several India-focused pre-IPO opportunities were available at valuations implying single-digit EV to EBITDA multiples due to global risk aversion. One Singapore-based NRI consortium invested in a profitable engineering and services firm that was listed in 2022. The company’s revenue CAGR exceeded 25% post-investment, and EBITDA margins expanded by over 400 basis points. Pre-IPO investors saw a multiple of invested capital exceeding 5x within three years of entry, net of fees and holding costs.

Family offices are scaling this logic. EY’s India Family Office Survey shows over 45% of India-linked family offices now allocate to private equity and private credit, up from under 25% in 2018. Average target allocation ranges between 15 and 30%, with holding periods exceeding seven years. These investors explicitly accept illiquidity in exchange for lower mark-to-market volatility and governance rights.

Currency management is often misunderstood. RBI data shows the INR depreciated at an average of roughly 3.2% annually against the USD between 2010 and 2024. However, depreciation is not linear and often coincides with global risk-off periods. For long-duration investors, unhedged exposure during growth phases can offset depreciation through higher local returns. Several NRI portfolios reviewed by private banks show lower realised volatility when currency hedging is applied tactically rather than permanently.

Flow data reinforces this behaviour. NSDL records indicate foreign portfolio investors sold over USD 15 billion of Indian equities in 2022. Domestic institutions absorbed much of this supply. By late 2023 and 2024, FPI flows turned positive again as earnings visibility improved. NRIs who deployed capital during outflow phases benefited from valuation compression rather than chasing momentum.

Vehicle selection remains critical. Direct equities offer liquidity but require discipline. Mutual funds provide diversification but mirror index drawdowns. AIFs and private vehicles offer structuring advantages, including downside protection, seniority, and governance, but come with lock-ins and fee drag. Tax treatment under DTAA provisions, particularly for NRIs in the US, UK, and Singapore, materially alters post-tax IRR and must be evaluated upfront.

Where Structure and Process Matter More Than Prediction

This is where experienced managers matter. Alpha AMC operates as a regulated India-focused asset manager offering structured exposure across public equities, private credit, and growth capital. For NRIs, the value proposition lies in compliance-aware onboarding, FEMA-aligned structures, and institutional-grade portfolio construction rather than aggressive return targeting. Alpha AMC’s blended approach aims to balance liquidity, income, and growth while respecting lock-in psychology and tax efficiency. This is an execution framework, not a return promise.

Across successful NRI portfolios, common patterns emerge. Capital is deployed gradually. Rebalancing is driven by cash flows rather than forecasts. Fees and tax leakage are monitored relentlessly. A 1% annual drag reduces terminal wealth by nearly 18% over 20 years. This arithmetic is not ignored by sophisticated investors.

Conclusion: Design Beats Forecasting

India’s growth path will not be smooth. Earnings cycles turn. Regulations evolve. Currency volatility persists. Yet India remains one of the few large economies where nominal growth, corporate profitability, and capital market depth are rising together. For NRIs with patience, regulatory awareness, and disciplined execution, this combination has delivered more resilient outcomes than global beta alone.

These are not speculative success stories. They are examples of allocation design, compliance-aware execution, and long-horizon thinking. In a world where volatility is global but growth is scarce, that distinction matters.

0

11

0

Publish Date

10 Feb 2026

Category

Ideas

Reading Time

6 mins

Social Presence

Table Of Content

Global Volatility Changed the Playbook for Offshore Investors

Execution, Not Timing, Separated Outcomes

Private Markets and Family Offices Are Scaling the Same Playbook

Where Structure and Process Matter More Than Prediction

Conclusion: Design Beats Forecasting

Tags

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2024–2025 Alpha. All rights reserved, Built with ❤️ in India