Introduction

India's major economy continues to grow at the fastest rate in the world as of February 2026. The IMF continues to predict medium-term growth in India above 6%, while the Reserve Bank of India projects FY26 GDP growth at 6.5 to 6.8%.

At the same time, India received the largest amount of remittances worldwide in 2023–2024, totalling over $125 Billion dollars. It's not just an impressive number; it stands for money that needs to be carefully considered.

The issue is that the majority of NRI investment advice still starts with a product. In actuality, capital has a purpose before it is allocated. Money has to grow. Some need to stabilise. Some people need to maintain their flexibility. And some people have to base their long-term choices on this. With that lens, here are the seven investment options that truly matter in 2026, backed by current data and grounded in how capital actually behaves.

Mutual Funds and Index Funds: The Behavioural Foundation

As of December 2025, India’s mutual fund industry stood at assets nearing the ₹80 lakh crore mark [4]. Systematic Investment Plans continue to contribute over ₹30,000 crore monthly, reflecting disciplined retail participation.

Over the past decade, the Nifty 50 has compounded at roughly 12 to 13% annually, while the broader Nifty 500 has delivered closer to 13 to 14%. For many NRIs, especially those early in their careers, this is the right starting point. Mutual funds do not demand constant monitoring. They reduce decision fatigue. They allow automatic investing even when life is in motion across geographies. They are not glamorous. But they compound quietly.

If your capital is below ₹3 crore and you are still building, this remains the cleanest way to participate in India’s structural growth without overcomplicating your life.

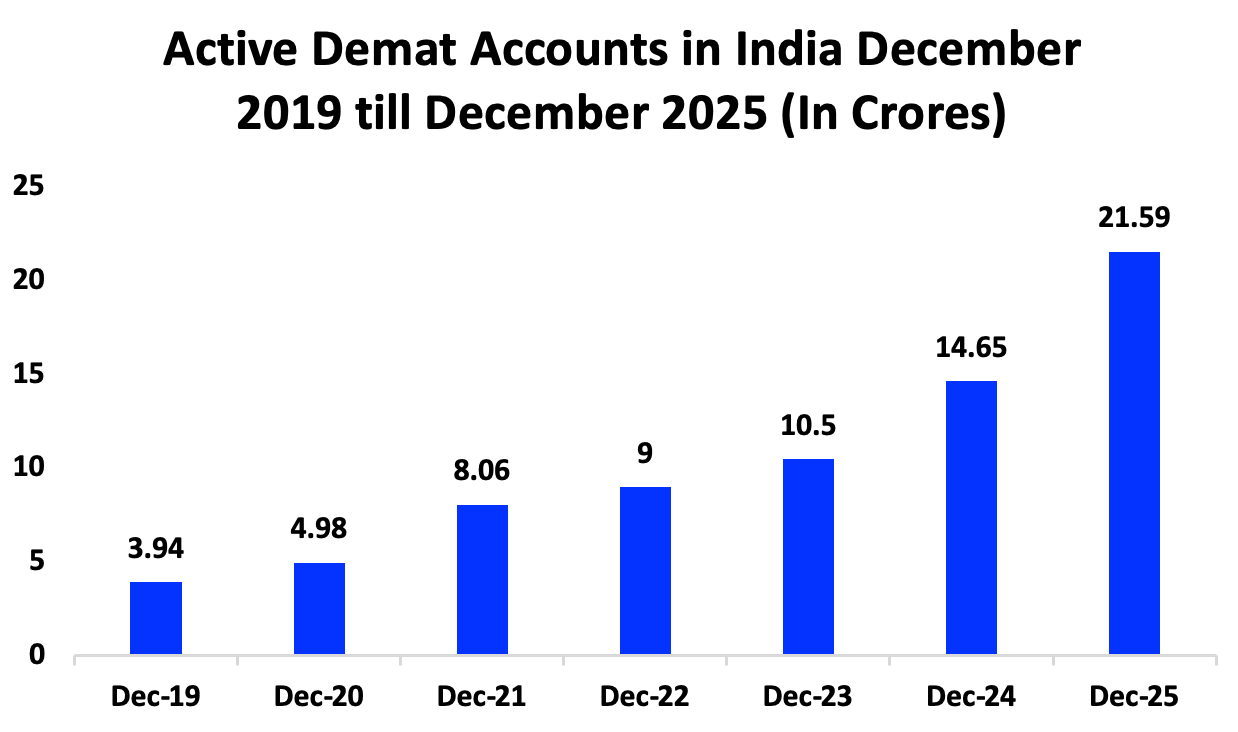

India now has more than 21 crore demat accounts, up 400% from 3.94 Cr in 2019, a reflection of deepening market participation. Access is no longer a barrier. Discipline still is. Indian equities typically exhibit annual volatility between 18 and 22%. Drawdowns of 15 to 25% are not unusual even in healthy cycles.

Direct stock investing is effective when there is a process, patience, and emotional capacity to ride through corrections. It is ineffective when it is a headline or social media-driven.

For NRIs with demanding careers and limited monitoring time, diversified equity holdings can be emotionally draining. Direct equities are effective only when the equity is surplus and conviction is earned through experience.

The PMS industry in India currently handles over ₹6.5 lakh crores as of late 2025[8]. The minimum ticket price usually starts at ₹50 lakh.

In contrast to mutual funds, the portfolio in PMS is more concentrated. The objective is not to be broadly diversified but to be ‘disciplined’ in conviction. According to a PMS Bazaar study covering performance data up to December 31, 2023, approximately 59% of PMS strategies outperformed their stated benchmarks over the prior five-year period. Several select PMS approaches delivered annualised returns above 20% over this timeframe, highlighting substantial performance dispersion and the importance of manager selection.

This is where discipline is outsourced. A good PMS imposes position sizing, cash allocation rules, and risk oversight that individual investors often struggle to maintain consistently. For portfolios between ₹3 crore and ₹10 crore, PMS can serve as a focused growth layer, provided the investor accepts volatility as part of the journey.

Residential real estate sales across India’s top cities approached ₹3.5 to ₹4 lakh crore in 2024, supported by end-user demand and improved balance sheets. Rental yields, however, remain modest. Residential yields typically range between 2 and 3%, while Grade A commercial assets offer closer to 6 to 8%.

For NRIs, property is rarely just a return calculation. It represents presence. It represents optionality. It sometimes represents a future return to India. The mistake is expecting real estate to generate high liquidity and high growth simultaneously. It is better understood as an anchor within a portfolio, not the engine of outperformance.

India’s listed REITs collectively manage assets worth tens of thousands of crores, and regulatory changes now allow banks to extend financing to REITs under defined norms, strengthening the ecosystem. Distribution yields generally range between 6 and 8 % annually.

Since India’s first REIT was listed in 2019, the sector has grown significantly. India now has four listed REITs with a total gross asset value nearing ₹1 lakh crore. This growth is mainly driven by Grade-A office parks in Bengaluru, Hyderabad, Mumbai, and NCR. Institutional interest has increased, and retail ownership has grown steadily through trading on the exchange.

In the last two years, listed REITs saw price fluctuations due to rising global interest rates, which generally affect yield-oriented assets. However, the overall operating performance has stayed fairly stable. This stability is due to strong leasing from Global Capability Centres (GCCs), high occupancy rates, and consistent rental increases. Distribution yields remain between 6% and 8%, making REITs sensitive to changes in interest rates, but they benefit from steady cash flows.

For NRIs who are interested in exposure to the story of commercial growth in India but do not want to be involved in tenant management or face complications related to distance, REITs emerge as a middle path. They provide income, liquidity, and institutional-grade assets in a regulated environment. This is particularly helpful for those who are not sure about their long-term decisions related to physical settlement.

Alternative Investment Funds: Institutional Participation in Private Growth

India’s AIF industry has grown meaningfully over the past five years. As of FY25, total commitments raised crossed approximately ₹15 lakh crore, with continued momentum into FY26. Category II AIFs, which include private equity and private credit, account for the largest share of this capital.

Private equity vintages in India have historically delivered top-quartile internal rates of return between 20 and 28%, with median returns often in the mid-teens, according to industry trackers such as Preqin [14]. Private credit funds have delivered net returns in the 11 to 14% range with lower mark-to-market volatility. These numbers explain why sophisticated investors are allocating more toward alternatives.

Alpha AMC’s Venture X Fund, structured under Category I AIF, focuses on growth-stage Indian businesses aligned with long-term domestic themes such as consumption formalisation, digital adoption, and scalable services. Under SEBI regulations, Category I funds typically invest in early-stage, innovation-led, and high-growth sectors that are considered economically desirable.

Unlike more mature private equity investments, Category I funds participate in the value chain at a point where the growth potential is greater but the dispersion of outcomes is also wider. The aim is not to maximise listing gains in the short term but to participate in companies before they become institutionalised public market names.

For patient NRIs with a 7 to 10 year horizon, Category I investments such as Venture X can offer asymmetric growth potential that is in sync with the structural growth of India.

NRE term deposit rates currently range between approximately 6.5% and 7.5%, depending on the tenure. With inflation near 5%, real returns are modest but stable.

Deposits remain critical for emergency reserves, short-term commitments, and psychological comfort. The mistake is allowing safety capital to dominate growth capital over long horizons. Stability should support ambition, not replace it.

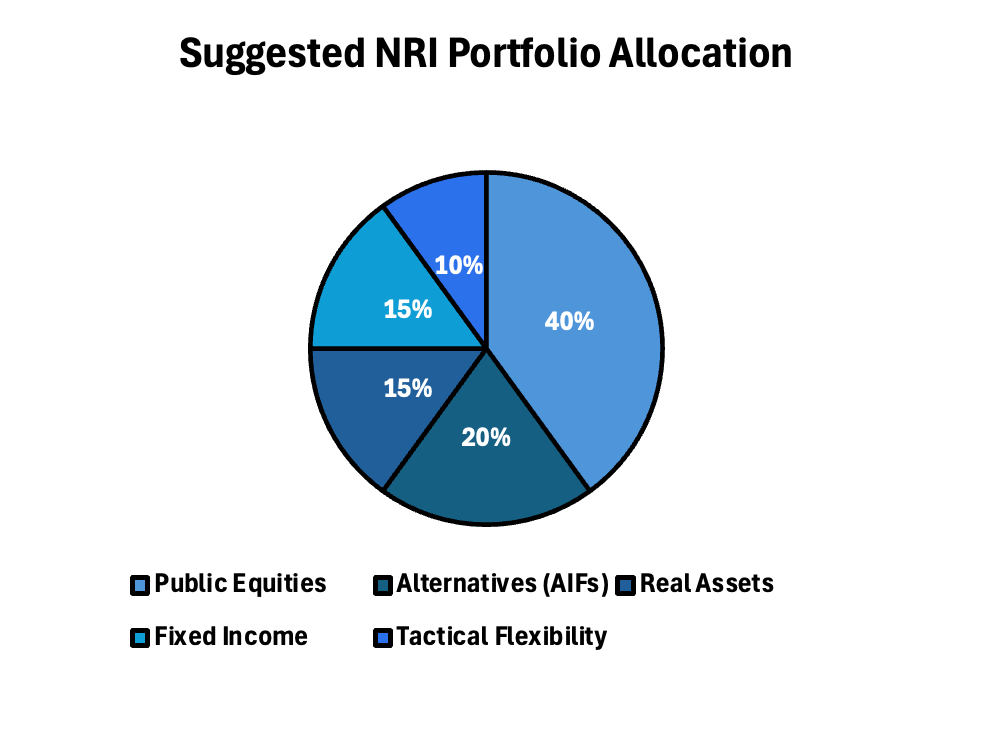

For NRIs with ₹5 to ₹15 crore net worth, a balanced approach may look like:

40 % public equities

20 % alternatives

15 % real assets

15 % fixed income

10 % tactical flexibility

For amounts above ₹25 crore, alternatives may extend to 30 to 40%, indicating a higher ability to sustain long-duration capital. The message is clear. Public markets offer liquidity and access. Alternatives offer structural alpha. Real estate is the anchor. Fixed income is the stabiliser.

Final Thought

In 2026, the debate is not about which asset class is superior. Every asset class addresses a different need.

Mutual funds create momentum.

Direct equities create conviction.

PMS creates discipline.

Real estate creates stability.

REITs create income flexibility.

Category II AIFs create long-term structural investment.

Deposits create safety.

Commodities, especially gold, mainly serve as macro hedges instead of being long-term wealth builders. Because of this, they are not seen as primary sources of wealth in this context. However, in a situation marked by geopolitical uncertainty, inflation cycles, and changes from central banks, a small investment in gold can add resilience to a portfolio and help spread out risk.

The Indian economy is on a strong track. Private capital formation is on the upswing. Institutional infrastructure is developing. NRIs today have access to investment options that were previously unavailable to them.

The benefit is not in seeking the maximum return. The benefit is in aligning resources with intentions.

When allocation is based on life cycles, liquidity requirements, and emotional risk profiles, results become more natural. That is the true paradigm shift for 2026.

0

12

0

Publish Date

02 Mar 2026

Category

Ideas

Reading Time

8 mins

Social Presence

Table Of Content

Introduction

Mutual Funds and Index Funds: The Behavioural Foundation

Alternative Investment Funds: Institutional Participation in Private Growth

Final Thought

Tags

AIF

NRI

mutualfunds

NRIINVESTING

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2024–2025 Alpha. All rights reserved, Built with ❤️ in India