Introduction

India’s alternative industry has shifted from a peripheral allocation to an institutional core. As pricing efficiency increases in public markets, allocators are evaluating private capital structures regulated by the Securities and Exchange Board of India (SEBI) under the AIF Regulations, 2012. The Indian AIF ecosystem has scaled rapidly over the past decade, both in terms of commitments and deployment, making category-level comparisons essential for informed allocation.

Industry Scale and Capital Distribution

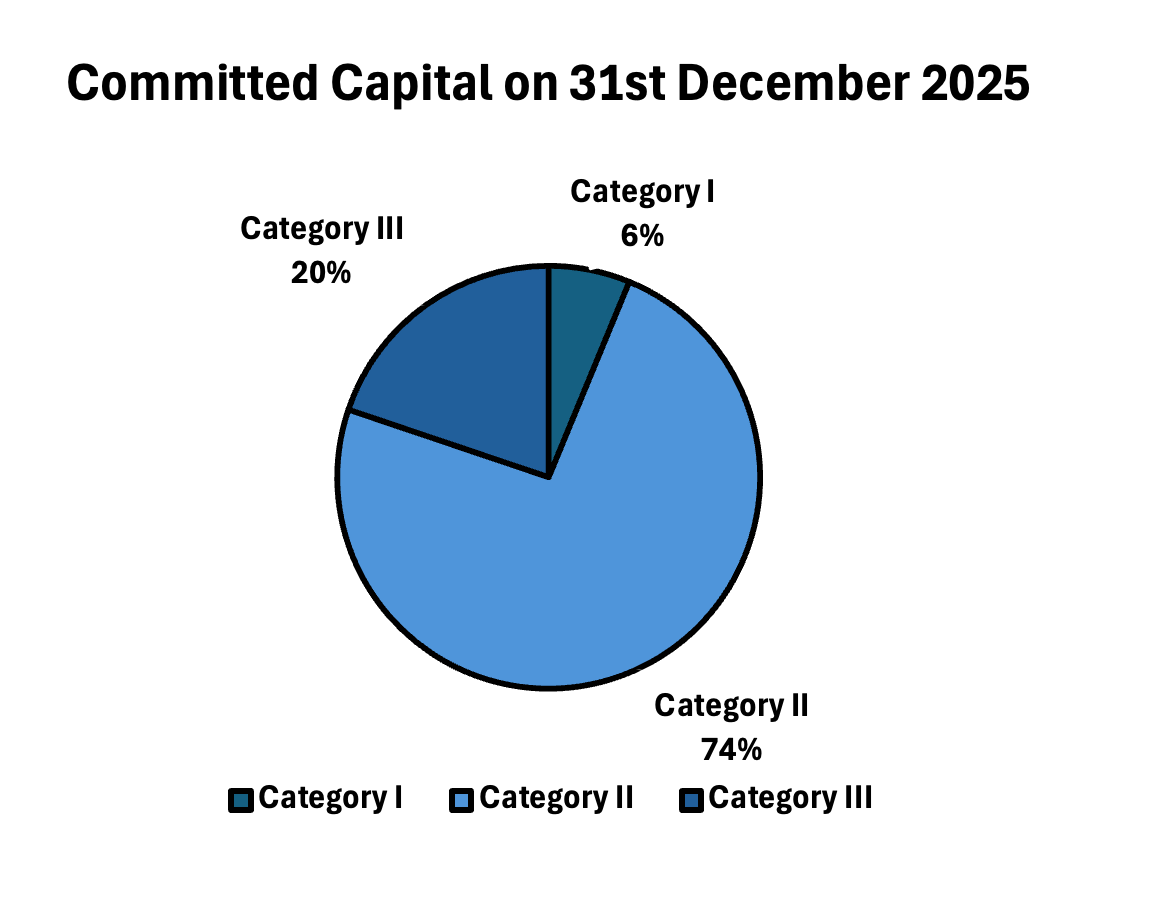

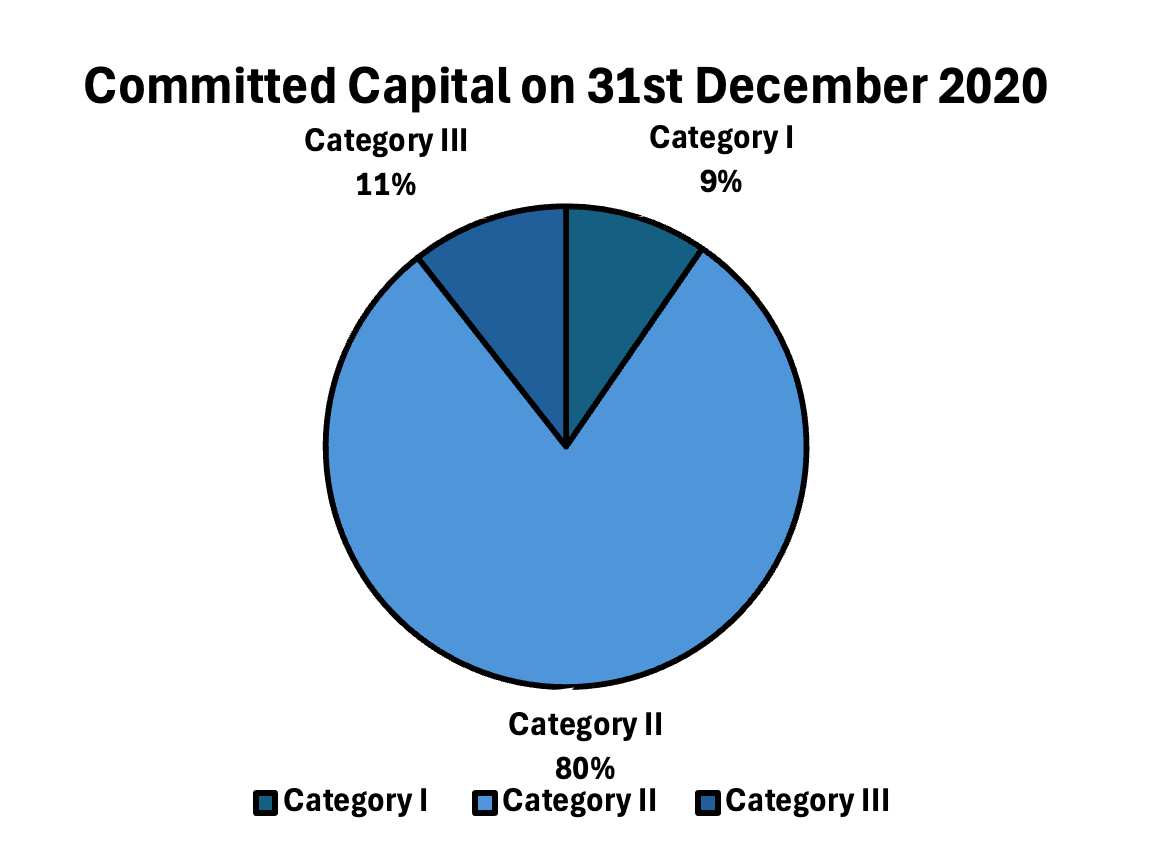

According to SEBI’s cumulative commitments raised investment data, total commitments raised across AIFs stand at ₹15,74,050 crore. Category-wise deployment is as follows:

Category I: ₹97,988 crore

Category II: ₹11,64,118 crore

Category III: ₹3,11,944 crore

Category II accounts for more than half of deployed capital. Category III represents nearly 20%, reflecting tactical hedge-style demand. Category I remains under 10%, concentrated in venture and SME capital formation.

Category Architecture and Investment Mandate

Category I AIF

Focus sectors include venture capital, SME, infrastructure and social enterprises. Leverage is prohibited. Minimum tenure generally ranges between five and seven years. Returns are driven by early-stage valuation inefficiencies, operating scale and institutionalisation.

Category II AIF

Includes private equity, growth capital and private credit strategies. Leverage is not structurally permitted. Tenure typically extends six to eight years. Value creation is operational and financial, combining earnings growth with exit optimisation.

Category III AIF

Covers long-short equity, arbitrage, structured credit and hedge-style strategies. Leverage is allowed. Tenure usually ranges from one to three years. Returns are market-linked and dependent on volatility and tactical positioning.

Benchmark data from Preqin and CRISIL AIF sub-category reports indicate the following illustrative gross IRR ranges:

Category I: 15% to 25% with wide dispersion

Category II: 18% to 28% for top-quartile funds

Category III: 5% to 20% annualised, depending on leverage and strategy[2][3]

Dispersion is materially higher in Categories I and III relative to Category II. Median performance in venture-style funds tends to lag the top quartile by significant margins, reflecting manager-dependent outcomes.

Category I and II funds follow drawdown models. Capital is committed upfront but deployed over two to four years. Full realisation may take six to eight years. Liquidity is limited until exit events occur.

Category III funds allow periodic redemption windows but are exposed to mark-to-market volatility. Drawdowns in volatile equity cycles can exceed 20% depending on leverage structure.

Illiquidity premium in Category I and II compensates for capital lock-in but increases reliance on exit timing.

Institutional allocators increasingly evaluate:

TVPI (Total Value to Paid-In Capital)

PME (Public Market Equivalent)

Maximum drawdown

Vintage year dispersion

Category II funds historically show stronger DPI visibility by year five relative to venture-style Category I funds, where realisations may cluster later in the fund life.

Category III funds exhibit higher short-term volatility but faster capital recycling.

India’s lower mid-market enterprise value range, between ₹100 crore and ₹1,000 crore, remains under-researched relative to large-cap equities. Earnings growth in these segments frequently exceeds 20% CAGR, while valuation multiples remain discounted due to limited liquidity.

Category II managers deploy structured growth capital, enhance governance, optimise capital allocation and pursue IPO or strategic exits. Exit ecosystem maturity has improved with SME IPO platforms and increasing M&A activity.

Operational value creation rather than multiple expansion alone underpins stronger risk-adjusted performance.

Category I, particularly SME-focused strategies, operates earlier in the growth curve. India’s MSME sector contributes approximately 30% to GDP and 45% to exports, yet institutional equity penetration remains limited.

SME-focused Category I managers can invest at valuation discounts before institutional scaling. Dispersion is high; however, asymmetry exists when underwriting is disciplined and governance intervention is structured.

At Alpha AMC, based in Gurugram, the strategy centres on identifying scalable SME businesses with operating leverage and durable earnings visibility. The emphasis is on research depth, promoter alignment and structured capital support rather than momentum-led entry. Operating within SEBI’s Category I framework allows focused exposure to segments where inefficiencies remain pronounced.[4]

Vintage year selection significantly influences realised IRR. Funds raised during high-liquidity cycles deploy at elevated multiples, compressing future returns. Funds raised during market corrections often secure attractive entry valuations.

Multi-vintage allocation reduces timing risk. Deployment pacing, follow-on reserve ratios and sector concentration must be evaluated at the commitment stage.

Typical structures include:

Management fee: 1.5% to 2%

Carried interest: 15% to 20% above hurdle

Hurdle rate: 8% to 10%

European waterfall structures protect LP capital by ensuring full capital return before carry distribution. Net IRR often compresses 300 to 500 basis points from gross IRR, depending on fee terms.

Alignment through GP commitment materially improves incentive symmetry.

Return Consistency: Category II highest

Asymmetric Upside: Category I highest

Liquidity Flexibility: Category III highest

Volatility: Category III highest

Capital Lock-In: Category I and II highest

Allocation Framework for Sophisticated Investors

For a 20% alternatives allocation:

50% to 60% Category II

20% to 30% Category I

10% to 20% Category III

Within Category I, manager selection is critical. Emphasis should be placed on sourcing capability, governance oversight, exit planning and promoter partnership. SME investing requires deep bottom-up diligence and sector-specific insight.

Alpha AMC’s SME-focused mandate positions it by targeting scalable businesses before valuation expansion; the strategy seeks to capture structural inefficiency rather than cyclical momentum.

No AIF category universally delivers the highest returns across all cycles. Category II offers the strongest track record of consistent institutional performance driven by operational value creation. Category I provides an asymmetric opportunity in undercapitalised SME segments when manager underwriting is rigorous. Category III delivers tactical alpha but with higher volatility sensitivity.

For investors seeking durable private market exposure in India, disciplined allocation across categories, combined with manager-specific diligence, remains the optimal approach. Structural inefficiency, governance alignment and patient capital determine outcomes more than the regulatory label alone.

0

14

0

Publish Date

16 Feb 2026

Category

Ideas

Reading Time

5 mins

Social Presence

Table Of Content

Introduction

Industry Scale and Capital Distribution

Category Architecture and Investment Mandate

Allocation Framework for Sophisticated Investors

Tags

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2024–2025 Alpha. All rights reserved, Built with ❤️ in India